If you’re a homeowner in Indiana and you’ve built up some equity in your house, you might be wondering: Can I borrow more on my existing mortgage? The answer could be yes — through what’s often called a top up mortgage.

Whether you need funds for home improvements, debt consolidation, college tuition, or unexpected expenses, a mortgage top up in Indiana can be a smart way to access extra money at potentially lower interest rates than credit cards or personal loans.

In this guide, we’ll break it all down in simple terms — what a top up mortgage is, how it works in Indiana, the pros and cons, and how to decide if it’s the right move for you.

Let’s dive in.

Table of Contents

What Is a Top Up Mortgage?

A top up mortgage is when you borrow additional money on top of your existing home loan. Instead of taking out a completely separate loan, you increase the amount of your current mortgage (or refinance to a higher amount) and receive the extra cash.

In the U.S., including Indiana, this is typically done in one of three ways:

- Cash-out refinance

- Home equity loan

- Home equity line of credit (HELOC)

Even though “top up mortgage” isn’t always the official term lenders use in Indiana, the concept is widely available through these options.

If your home has increased in value or you’ve paid down a significant portion of your loan, you may have built enough equity to qualify.

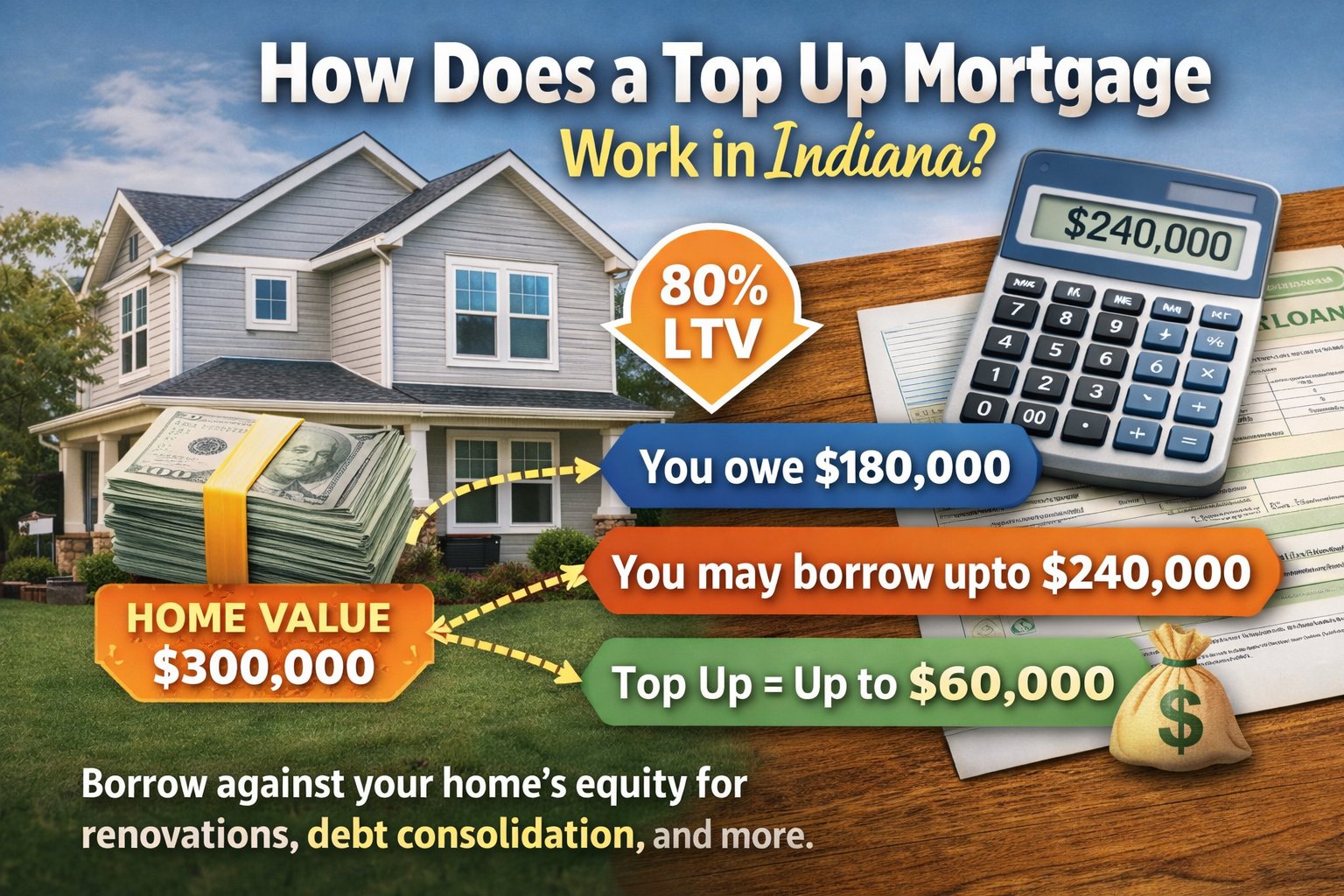

How Does a Top Up Mortgage Work in Indiana?

Let’s say your home in Indianapolis is worth $300,000. You currently owe $180,000 on your mortgage.

That means you have $120,000 in equity.

Most Indiana lenders allow you to borrow up to 80% to 85% of your home’s value, depending on your credit profile and loan type.

If your lender allows 80%:

- 80% of $300,000 = $240,000

- You owe $180,000

- You may be able to borrow up to $60,000 as a mortgage top up

That $60,000 can be used for almost anything — renovations, medical bills, business investments, or even paying off higher-interest debt.

Why Indiana Homeowners Consider a Mortgage Top Up

You’re not alone if you’re thinking about tapping into your home’s equity. Many Indiana homeowners explore this option for practical reasons.

Here are the most common ones:

1. Home Improvements

Planning to upgrade your kitchen, finish your basement, or add a deck for those Indiana summer evenings? Using a top up mortgage for home renovations can increase your property value while improving your quality of life.

2. Debt Consolidation

If you’re juggling credit cards with high interest rates, a mortgage top up could help you consolidate debt into one lower monthly payment.

3. Education Costs

College tuition isn’t cheap. Some homeowners use their home equity to help fund education expenses.

4. Emergency Expenses

Unexpected medical bills or major repairs happen. Having access to your equity can provide financial breathing room.

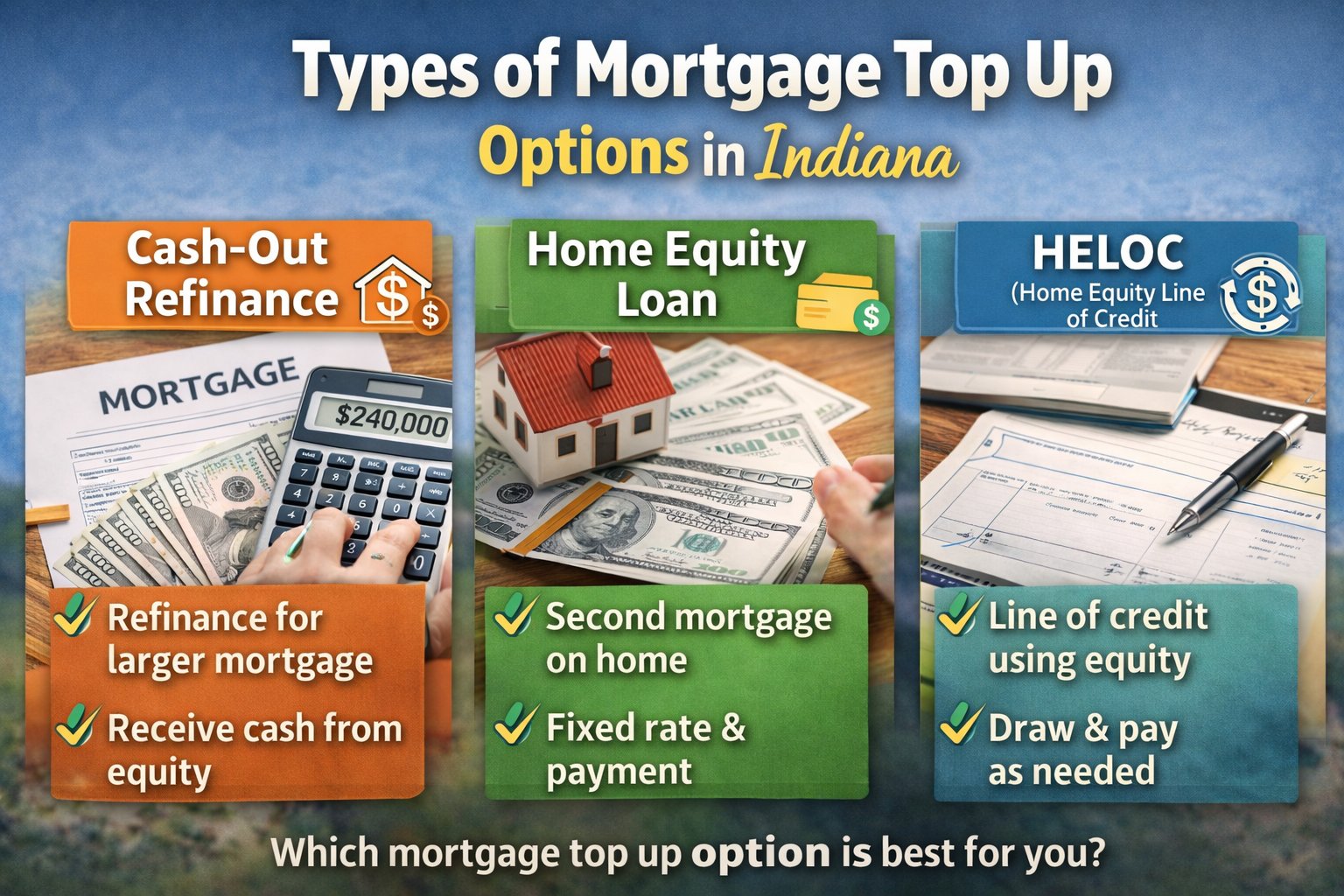

Types of Mortgage Top Up Options in Indiana

Let’s break down your main options.

1. Cash-Out Refinance

This is the most common way to top up a mortgage in Indiana.

You refinance your existing mortgage for a larger amount and receive the difference in cash.

Pros:

- Potentially lower interest rates

- One single monthly payment

- Fixed interest rate option available

Cons:

- Closing costs apply

- Your loan term may restart (e.g., another 30 years)

This option works best if current mortgage rates are similar to or lower than your existing rate.

2. Home Equity Loan

A home equity loan is a second mortgage with a fixed interest rate and fixed monthly payments.

Pros:

- Predictable payments

- Fixed rate protection

Cons:

- Two separate monthly payments

- Uses your home as collateral

This is often ideal if you need a lump sum and want structured repayment.

3. HELOC (Home Equity Line of Credit)

A HELOC works more like a credit card. You’re approved for a maximum amount and borrow as needed.

Pros:

- Flexible borrowing

- Only pay interest on what you use

Cons:

- Variable interest rates

- Payments can increase over time

HELOCs are popular in Indiana for ongoing renovation projects.

Requirements for a Top Up Mortgage in Indiana

Before applying, here’s what lenders typically look at:

✔ Home Equity

You generally need at least 15% to 20% equity in your home.

✔ Credit Score

Most lenders prefer:

- 620+ for conventional loans

- Higher scores for better rates

✔ Debt-to-Income Ratio (DTI)

Your total monthly debt payments (including the new loan) should typically be under 43% of your income.

✔ Stable Income

You’ll need proof of employment and steady income.

Pros and Cons of a Top Up Mortgage

Let’s be honest — this isn’t a one-size-fits-all solution.

Benefits

- Lower interest rates compared to credit cards

- Access to large loan amounts

- Potential tax advantages (consult a tax professional)

- Can increase home value if used for renovations

Risks

- Your home is collateral

- Longer repayment period

- Closing costs and fees

- Risk of foreclosure if payments aren’t made

It’s important to weigh the risks carefully.

Indiana Housing Market Considerations

Indiana’s real estate market has seen steady growth in many cities like:

- Indianapolis

- Fort Wayne

- Evansville

- Carmel

- Fishers

Rising home values mean many homeowners have more equity than they realize.

However, market conditions change. Before applying for a mortgage top up in Indiana, consider:

- Current mortgage interest rates

- Local property value trends

- Your long-term financial goals

How to Apply for a Top Up Mortgage in Indiana

Here’s a simple step-by-step guide:

Step 1: Check Your Equity

Look at your mortgage balance and estimated home value.

Step 2: Review Your Credit

Check your credit score and fix any errors before applying.

Step 3: Compare Lenders

Shop around with:

- Local Indiana banks

- Credit unions

- Online mortgage lenders

Ask about:

- Interest rates

- Closing costs

- Loan terms

- Prepayment penalties

Step 4: Get a Home Appraisal

Most lenders require an appraisal to confirm your home’s value.

Step 5: Close the Loan

Once approved, you’ll sign documents and receive your funds.

Is a Top Up Mortgage in Indiana Right for You?

Ask yourself:

- Do I have enough equity?

- Can I comfortably afford the higher payment?

- Am I using the funds for something financially responsible?

- Would another loan option be cheaper?

If you’re using the money to improve your home or eliminate high-interest debt, it can be a smart move.

If it’s for luxury spending or non-essential purchases, you may want to reconsider.

Smart Tips Before You Commit

Here are a few practical tips:

💡 Don’t Borrow the Maximum Just Because You Can

Leave yourself a cushion.

💡 Understand the Total Cost

Look beyond the interest rate — factor in fees and closing costs.

💡 Keep Emergency Savings

Don’t drain your financial safety net.

💡 Consider Future Plans

Planning to move soon? A refinance might not make sense.

Frequently Asked Questions About Top Up Mortgage in Indiana

Is a top up mortgage the same as refinancing?

Not exactly. A cash-out refinance is one form of topping up your mortgage.

Can I top up my FHA mortgage?

Yes, through an FHA cash-out refinance, if you meet eligibility requirements.

How long does approval take?

Typically 2 to 6 weeks, depending on the lender.

Are there closing costs?

Yes. Expect 2% to 5% of the loan amount in most cases.

Final Thoughts

A top up mortgage in Indiana can be a powerful financial tool when used wisely. It gives you access to your home’s equity — often at lower rates than other borrowing options.

But remember, your home is on the line.

Take time to compare lenders, run the numbers, and think long-term. If the numbers make sense and the purpose is solid, it can be a smart way to leverage the value you’ve built in your property.

If you’re unsure, consider speaking with a local Indiana mortgage advisor who understands your market.

You’ve worked hard to build equity in your home — make sure you use it in a way that strengthens your financial future, not weakens it.