Buying a home is one of the biggest financial decisions most people will ever make. If you’re planning to purchase a home in Indiana, you’ve probably come across different types of mortgage options—fixed-rate, FHA, VA, jumbo loans, and of course, variable mortgages, often called adjustable-rate mortgages (ARMs).

At first glance, variable mortgages can look incredibly appealing. Lower starting rates, reduced initial monthly payments, and flexible terms—what’s not to like?

But like most things in finance, there’s more beneath the surface.

In this guide, we’ll walk through everything you need to know about variable mortgages in Indiana, including how they work, current market trends, pros and cons, risks, and whether they’re the right fit for you.

Table of Contents

What Is a Variable Mortgage?

A variable mortgage (or adjustable-rate mortgage) is a type of home loan where the interest rate changes over time instead of staying fixed for the entire loan period.

Unlike a traditional fixed-rate mortgage—where your interest rate and monthly payment remain the same—a variable mortgage starts with a fixed introductory period, followed by periodic adjustments.

These adjustments are based on:

- A financial index (like Treasury rates or SOFR)

- A fixed margin set by your lender

For example, you might have a 5/1 ARM:

- First 5 years: fixed rate

- After that: rate adjusts annually

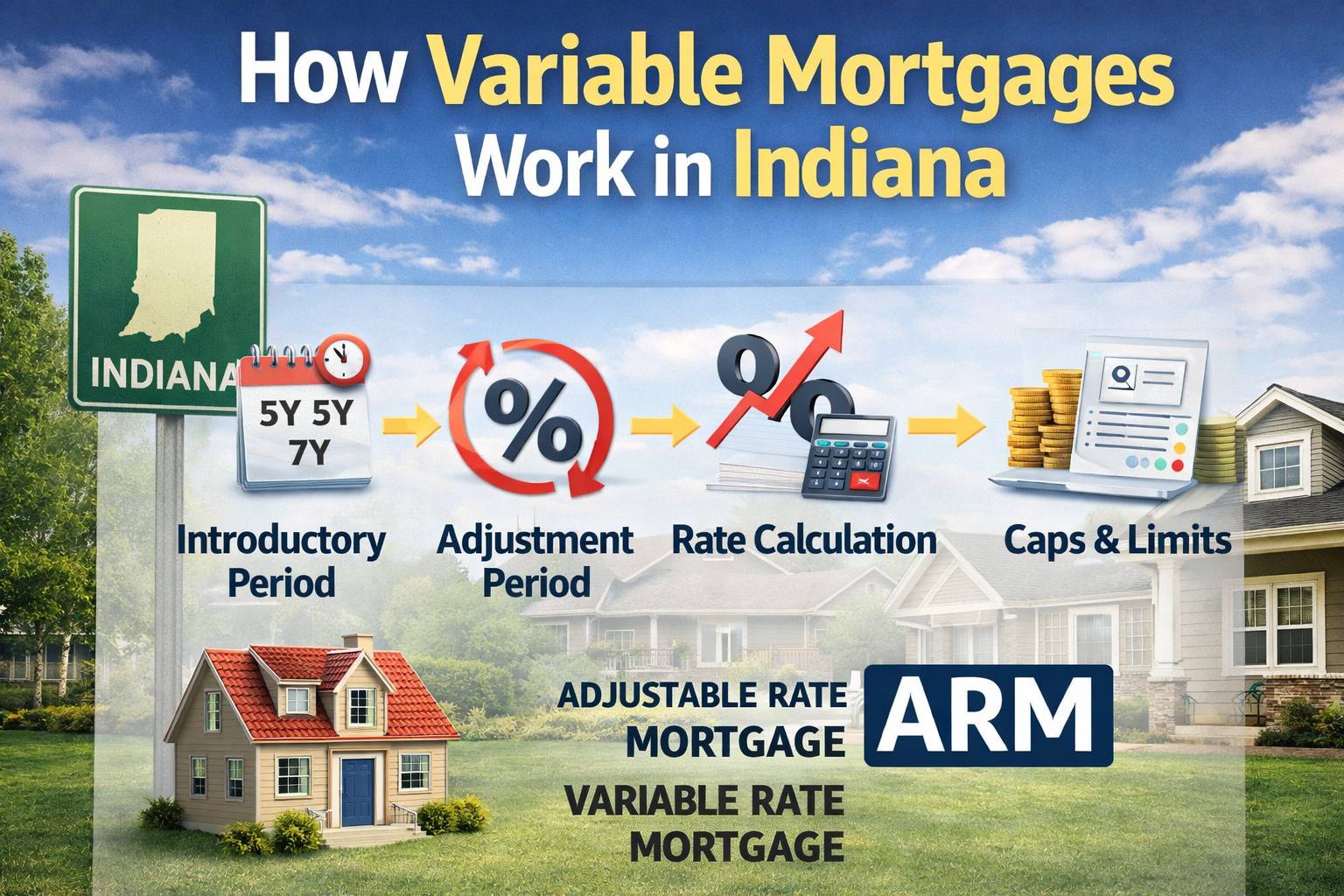

How Variable Mortgages Work in Indiana

In Indiana, variable mortgages operate similarly to those across the U.S., but local housing conditions and lender offerings can influence rates and terms.

Here’s how a typical ARM works:

1. Introductory Period

You start with a lower fixed rate than most fixed-rate mortgages. This period can last:

- 3 years

- 5 years

- 7 years

- 10 years

2. Adjustment Period

After the initial phase, your rate resets periodically—often every year.

3. Rate Calculation

Your new rate is calculated using:

- A benchmark index (market-based)

- Plus a lender margin

4. Caps and Limits

Most ARMs have:

- Rate caps (limit how much your rate can increase)

- Lifetime caps (maximum rate over the loan’s life)

Even with caps, your payments can still increase significantly.

Current Variable Mortgage Rates in Indiana (2026)

As of early 2026, mortgage rates in Indiana have been fluctuating but generally remain above 6% for fixed loans.

Here’s a snapshot of variable (ARM) rates:

- 3-year ARM: ~7.2%

- 5-year ARM: ~6.35%

- 7-year ARM: ~5.75%–6.04%

In some cases:

- 5/1 ARM rates are around 5.875%–6.125%

These rates are often lower than fixed-rate mortgages initially, which is why many buyers consider them.

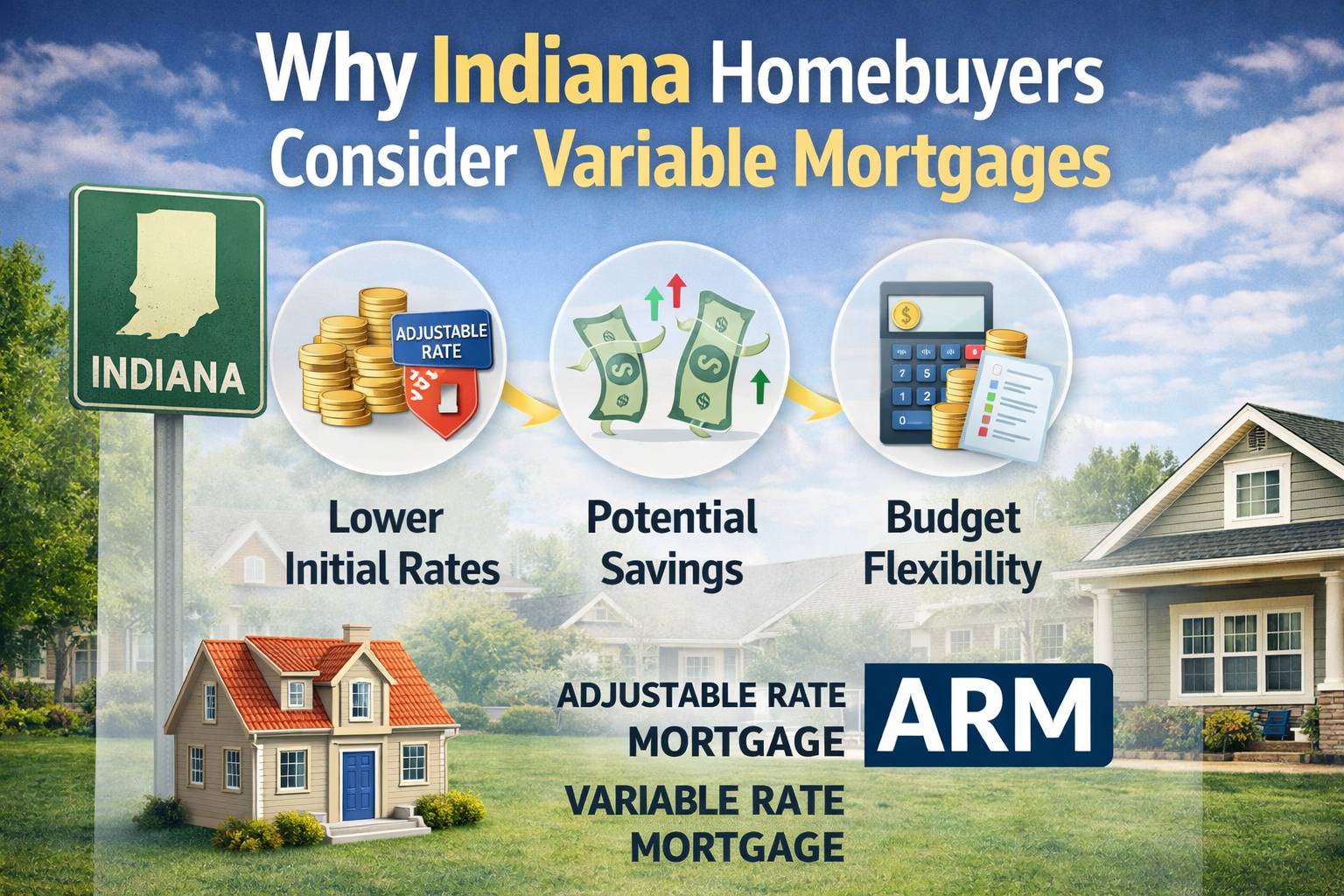

Why Indiana Homebuyers Consider Variable Mortgages

Indiana is known for relatively affordable housing compared to other states. The median home value is significantly lower than the national average, making homeownership accessible for many buyers.

Because of this, buyers often explore creative financing options, including ARMs, to maximize affordability.

Here are the main reasons people choose variable mortgages in Indiana:

1. Lower Initial Monthly Payments

This is the biggest draw.

Because the starting interest rate is lower, your monthly mortgage payment is also lower—at least in the beginning.

For example:

- A fixed loan might be 6.2%

- A 7-year ARM might be 5.8%

That difference can save hundreds of dollars per month early on.

2. Ideal for Short-Term Homeowners

If you plan to:

- Move within 5–7 years

- Upgrade homes

- Relocate for work

…then a variable mortgage can make sense.

You benefit from the low initial rate and sell before adjustments kick in.

3. Flexibility in a Changing Market

Some buyers use ARMs strategically, planning to:

- Refinance later

- Pay off early

- Sell before rates rise

This approach works best when you’re financially prepared and understand the risks.

4. Access to More Expensive Homes

Lower initial payments can increase your buying power.

This means you might qualify for a slightly higher-priced home compared to a fixed-rate mortgage.

The Risks of Variable Mortgages

Now let’s talk about the part many lenders don’t emphasize enough.

Variable mortgages are not inherently bad—but they shift risk from the lender to the borrower.

1. Payment Uncertainty

Your monthly payment can change—and sometimes dramatically.

When rates reset:

- Payments may increase significantly

- Budgeting becomes harder

For example, even a small rate increase can raise payments by hundreds of dollars.

2. Exposure to Market Conditions

ARM rates are tied to broader economic factors:

- Federal Reserve decisions

- Inflation

- Housing demand

If rates rise nationally, your mortgage cost increases too.

3. Long-Term Cost Can Be Higher

While you save money upfront, over time you might:

- Pay more interest

- End up with higher total loan costs

Especially if rates rise consistently.

4. Complexity

Compared to fixed-rate mortgages, ARMs are more complicated.

You need to understand:

- Adjustment schedules

- Rate caps

- Index benchmarks

Without this knowledge, it’s easy to underestimate future costs.

Understanding ARM “Resets” (The Critical Moment)

One of the most important concepts with variable mortgages is the reset.

A reset happens when your interest rate changes after the initial fixed period.

At that point:

- Your new rate is calculated

- Your monthly payment is updated

This can result in:

- A slight increase

- Or a significant jump

In Indiana, many ARMs reset annually after the initial term, depending on the loan structure.

Example: How a Variable Mortgage Can Change

Let’s say you take out a mortgage with:

- Initial rate: 5.5%

- Loan amount: $300,000

After 5 years, your rate adjusts to 7%:

- Monthly payment increases noticeably

- Total interest cost rises

If rates drop instead:

- Your payment could decrease

This uncertainty is the trade-off.

Fixed vs Variable Mortgages in Indiana

Let’s break it down simply:

| Feature | Fixed Mortgage | Variable Mortgage |

|---|---|---|

| Rate Stability | Fixed | Changes over time |

| Monthly Payment | Predictable | Can increase or decrease |

| Initial Rate | Higher | Lower |

| Risk Level | Low | Medium to High |

| Best For | Long-term homeowners | Short-term or flexible buyers |

Who Should Consider a Variable Mortgage?

A variable mortgage isn’t for everyone—but it can be a smart move if you fit certain profiles.

Good Candidates:

- First-time buyers planning to upgrade soon

- Investors flipping properties

- Professionals expecting income growth

- Buyers comfortable with financial risk

Not Ideal For:

- Fixed-income households

- Risk-averse buyers

- Long-term homeowners (10+ years)

- People with tight budgets

Strategies to Manage a Variable Mortgage

If you’re considering an ARM in Indiana, here are some smart strategies:

1. Plan for the Worst-Case Scenario

Always calculate:

- Maximum possible interest rate

- Maximum monthly payment

If you can’t afford that number, rethink the loan.

2. Build a Financial Cushion

Set aside savings to cover:

- Rate increases

- Unexpected expenses

3. Monitor Interest Rates

Stay informed about:

- Federal Reserve decisions

- Inflation trends

These directly affect ARM adjustments.

4. Consider Refinancing

If rates rise too much:

- Refinance into a fixed-rate mortgage

Many Indiana homeowners use this strategy.

5. Understand Your Loan Terms

Know:

- Adjustment frequency

- Rate caps

- Index used

This knowledge is crucial.

The Indiana Housing Market Context

Indiana remains one of the more affordable states for housing.

Key highlights:

- Lower median home prices

- Moderate cost of living

- Strong homeownership rates

However:

- Mortgage rates remain relatively high (above 6%)

- Economic uncertainty continues to affect borrowing costs

This makes ARMs attractive—but also risky.

Common Mistakes to Avoid

Let’s be honest—most people don’t fully understand variable mortgages when they sign.

Here are common pitfalls:

1. Focusing Only on the Initial Rate

That low rate is temporary.

Always look beyond the first 3–7 years.

2. Ignoring Rate Caps

Caps limit increases—but they don’t eliminate them.

3. Overestimating Future Income

Don’t assume:

- Promotions

- Raises

- Better financial conditions

Plan based on what you earn today.

4. Skipping Professional Advice

Always talk to:

- Mortgage advisors

- Financial planners

Final Thoughts: Is a Variable Mortgage Right for You?

Variable mortgages in Indiana can be a powerful financial tool—but only when used correctly.

They offer:

- Lower starting costs

- Greater flexibility

- Strategic opportunities

But they also come with:

- Uncertainty

- Risk

- Complexity

The key is understanding your situation.

If you’re planning to stay in your home long-term and want peace of mind, a fixed-rate mortgage may be the safer route.

If you’re flexible, financially prepared, and comfortable with some risk, a variable mortgage could save you money—at least in the short term.

Bottom Line

A variable mortgage isn’t “good” or “bad.”

It’s simply a tool.

And like any tool, its effectiveness depends on how—and when—you use it.

If you’re buying a home in Indiana, take the time to:

- Understand your options

- Run the numbers

- Think long-term

Because the best mortgage isn’t just the cheapest one today—it’s the one you can afford tomorrow.