If you own a home in Indiana, you might be sitting on a valuable financial resource without even realizing it—your home equity. Many homeowners are turning to a Home Equity Line of Credit (HELOC) as a flexible way to access funds for renovations, debt consolidation, emergencies, or major life expenses.

But how exactly does a home equity line of credit mortgage in Indiana work? Is it the right choice for you? And what should Indiana homeowners know before applying?

In this guide, we’ll walk through everything you need to know—from how HELOCs work to their benefits, risks, and tips for getting the best rates in Indiana.

Let’s dive in.

Table of Contents

What Is a Home Equity Line of Credit (HELOC)?

A Home Equity Line of Credit, often called a HELOC, is a type of loan that allows you to borrow money against the equity you’ve built in your home.

Think of it like a credit card that uses your house as collateral.

Instead of receiving a lump sum like a traditional loan, a HELOC provides a revolving line of credit. You can borrow what you need, repay it, and borrow again during the draw period.

For many homeowners in Indiana, this flexibility makes a HELOC one of the most practical financing options available.

Quick Example

Let’s say:

- Your home value: $300,000

- Mortgage balance: $180,000

- Equity: $120,000

Most lenders allow borrowing up to 80–85% of your home’s value.

So you might qualify for a HELOC of around $60,000–$75,000, depending on the lender and your financial profile.

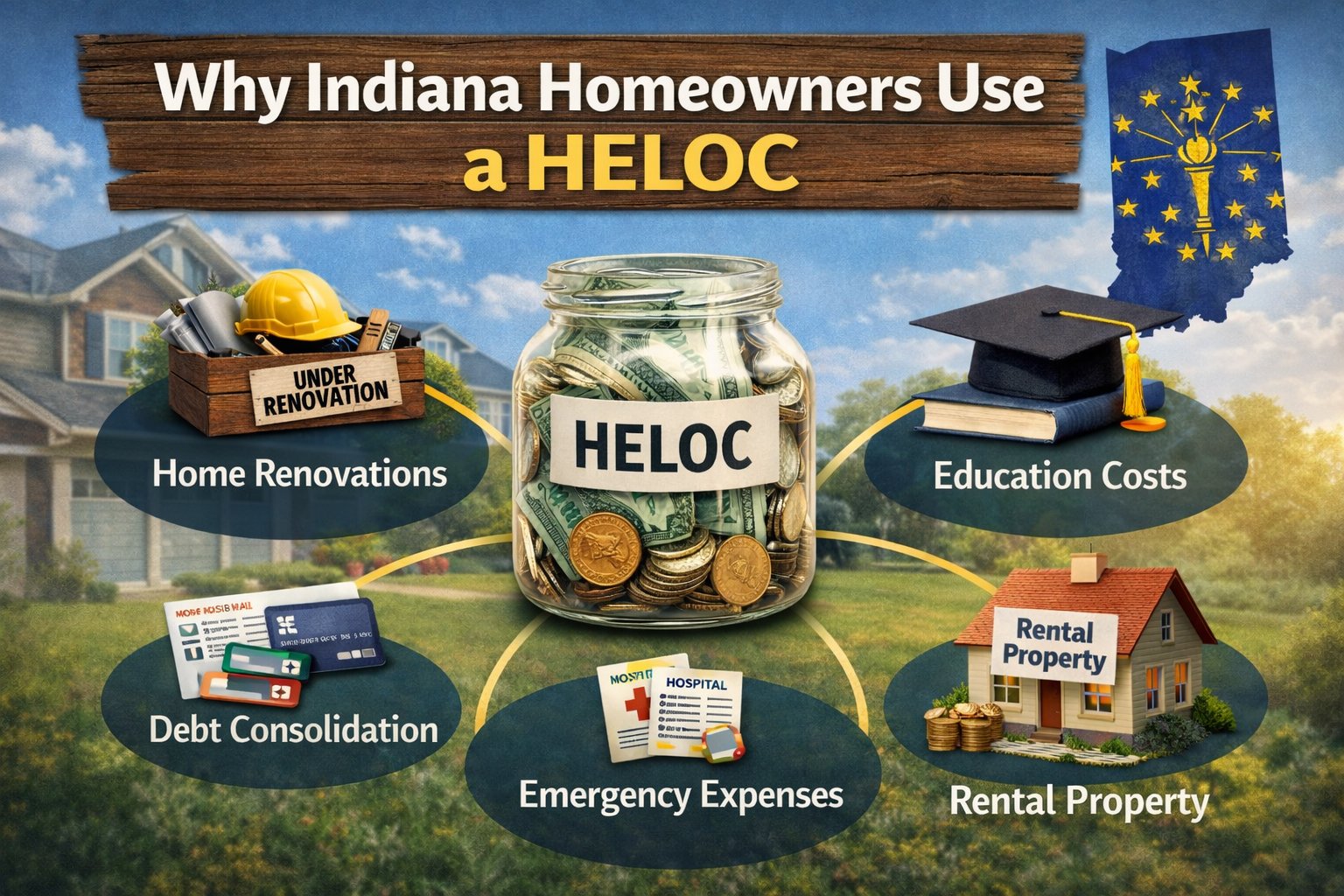

Why Indiana Homeowners Use a HELOC

Indiana homeowners often choose a home equity line of credit mortgage for its flexibility and relatively lower interest rates compared to personal loans or credit cards.

Here are the most common reasons people apply for a HELOC.

1. Home Renovations

One of the most popular uses of a HELOC in Indiana is home improvement projects.

Projects like:

- Kitchen remodels

- Bathroom upgrades

- New roofing

- Basement finishing

- Energy-efficient upgrades

Not only can these improvements enhance your quality of life, but they may also increase your home’s value.

Many homeowners prefer a HELOC because they can withdraw funds as needed instead of borrowing everything upfront.

2. Debt Consolidation

If you’re dealing with high-interest credit card debt, a HELOC may help reduce your interest payments.

For example:

Credit cards often carry interest rates of 20% or more, while HELOC rates may be significantly lower.

By consolidating debt into a home equity line of credit mortgage in Indiana, you might simplify your payments and potentially save thousands in interest.

However, it’s important to remember that your home becomes collateral, so responsible repayment is crucial.

3. Emergency Expenses

Life is unpredictable.

Medical bills, unexpected repairs, or temporary income loss can strain finances.

A HELOC can act as a financial safety net, giving homeowners access to funds when they need them most.

4. Education Costs

Some Indiana families use HELOC funds to help cover college tuition or education expenses.

While federal student loans often have protections, a HELOC may offer lower interest rates in certain situations.

Still, it’s important to weigh the risks since the loan is tied to your home.

5. Real Estate Investments

Some homeowners leverage their equity to invest in rental properties or real estate opportunities.

Using a HELOC as a source of capital allows investors to move quickly when opportunities arise.

How a HELOC Mortgage Works in Indiana

Understanding how the structure works can help you decide whether it fits your financial goals.

A typical home equity line of credit mortgage in Indiana has two main phases:

1. Draw Period

This period usually lasts 5 to 10 years.

During this time:

- You can borrow money from your credit line

- You can repay and borrow again

- Payments may be interest-only

This flexibility is why many homeowners choose a HELOC over traditional loans.

2. Repayment Period

After the draw period ends, the repayment phase begins.

This typically lasts 10 to 20 years.

During repayment:

- You can no longer withdraw funds

- Payments include principal and interest

- Monthly payments may increase

Planning for this transition is important so there are no surprises later.

HELOC vs Home Equity Loan in Indiana

Many homeowners confuse a HELOC with a home equity loan, but they work differently.

Here’s a simple comparison.

| Feature | HELOC | Home Equity Loan |

|---|---|---|

| Payment Structure | Revolving credit line | Lump sum |

| Interest Rate | Usually variable | Often fixed |

| Flexibility | Very flexible | Less flexible |

| Best For | Ongoing expenses | One-time expenses |

If you need funds gradually, a HELOC mortgage in Indiana is usually the better choice.

If you need a fixed amount for a single project, a home equity loan may be more suitable.

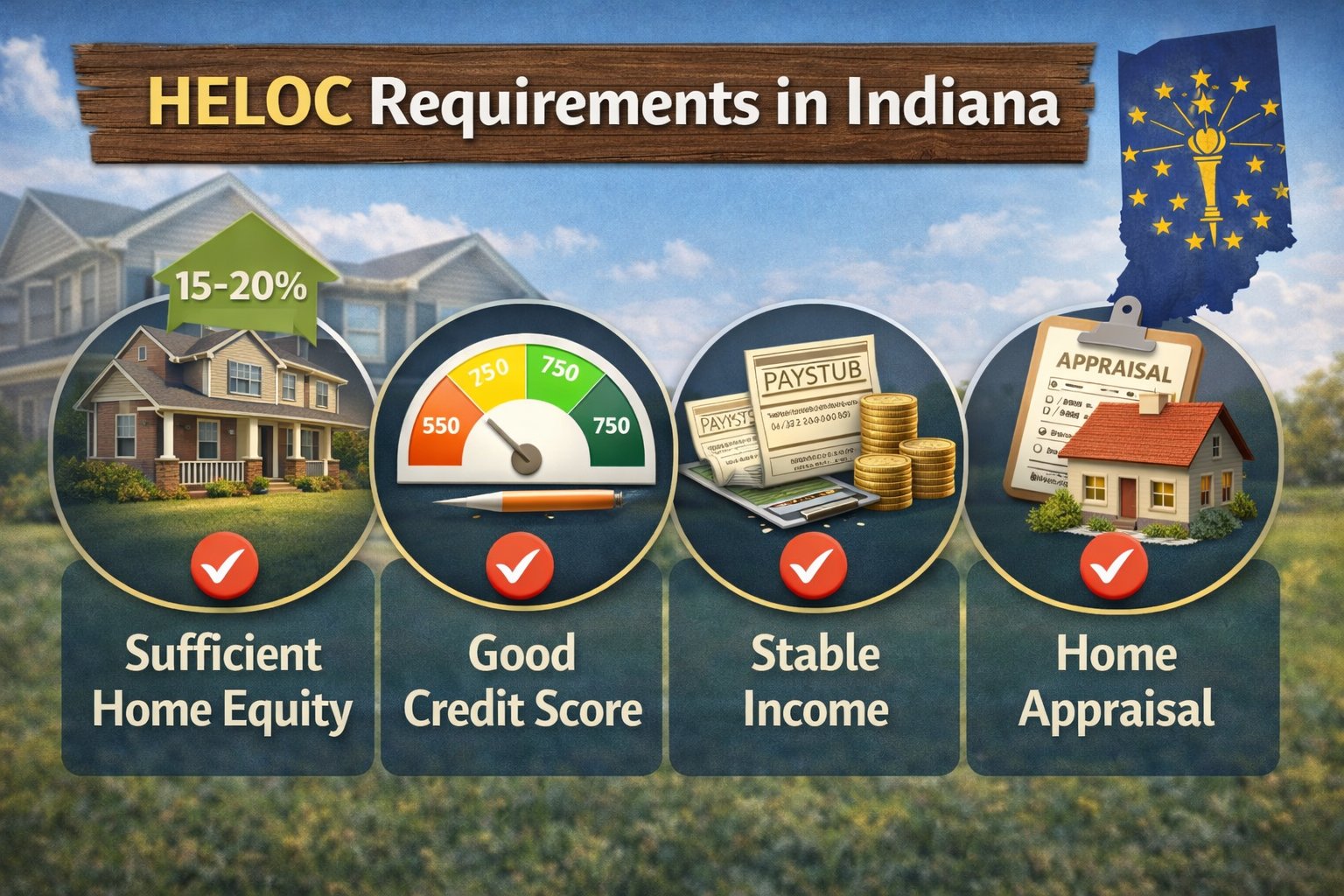

HELOC Requirements in Indiana

While exact requirements vary by lender, most Indiana lenders look for several key factors when approving a home equity line of credit.

1. Sufficient Home Equity

Most lenders require at least 15–20% equity in your home.

The more equity you have, the larger your potential credit line.

2. Good Credit Score

While requirements vary, many lenders prefer:

- 620 minimum credit score

- 700+ for best rates

Better credit usually means lower interest rates.

3. Stable Income

Lenders want to see that you can repay the loan.

They will review:

- Employment history

- Income documentation

- Debt-to-income ratio

4. Appraisal of Your Home

In many cases, lenders require a home appraisal to determine your property’s current market value.

This helps calculate how much equity you can access.

Current HELOC Rates in Indiana

Interest rates for a home equity line of credit mortgage in Indiana can vary depending on several factors:

- Credit score

- Loan amount

- Property value

- Market conditions

- Lender policies

Most HELOCs have variable interest rates, meaning the rate may change over time based on market conditions.

That’s why it’s always a good idea to compare multiple lenders before making a decision.

Advantages of a HELOC for Indiana Homeowners

There are several reasons why HELOCs have become popular financing tools.

Flexible Borrowing

You borrow only what you need when you need it.

This can reduce unnecessary interest payments.

Lower Interest Rates

Compared to credit cards or personal loans, HELOCs typically offer lower interest rates.

Potential Tax Benefits

In some situations, interest paid on a HELOC used for home improvements may be tax-deductible.

Always consult a tax professional for guidance.

Large Borrowing Limits

Because your home secures the loan, you may qualify for larger credit lines than other financing options.

Risks of a Home Equity Line of Credit

While HELOCs offer advantages, they also come with risks.

Understanding these risks helps you make informed financial decisions.

Your Home Is Collateral

If you fail to repay the loan, the lender could foreclose on your home.

That’s why careful financial planning is important.

Variable Interest Rates

Many HELOCs have variable rates, which means your payment may increase if interest rates rise.

Overborrowing

Because HELOC funds are easy to access, some homeowners borrow more than they actually need.

Treating the credit line responsibly is essential.

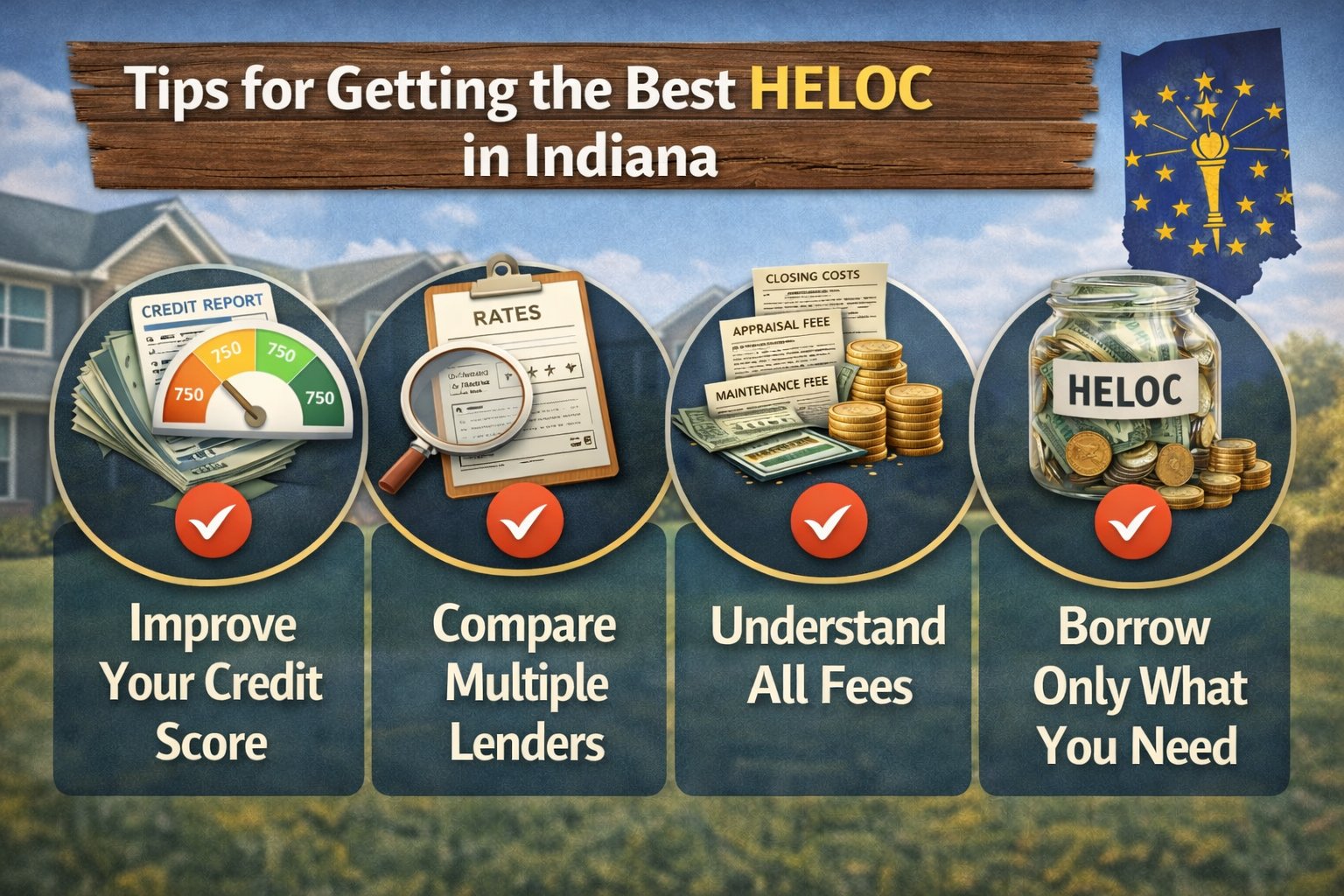

Tips for Getting the Best HELOC in Indiana

If you’re considering applying for a home equity line of credit mortgage in Indiana, these tips can help you secure better terms.

1. Improve Your Credit Score

Even a small credit score increase can help you qualify for lower interest rates.

Paying down credit cards and making on-time payments can help.

2. Compare Multiple Lenders

Different lenders may offer different rates, fees, and credit limits.

Consider checking:

- Banks

- Credit unions

- Online lenders

Shopping around can save you thousands.

3. Understand All Fees

Some HELOCs include:

- Appraisal fees

- Closing costs

- annual maintenance fees

Make sure you review all costs before signing.

4. Borrow Only What You Need

Just because you have access to a large credit line doesn’t mean you need to use it all.

Borrow responsibly to protect your finances.

Best Lenders Offering HELOCs in Indiana

While options change over time, some lenders commonly offering HELOC products include:

- Local Indiana credit unions

- Regional banks

- National banks

- Online mortgage lenders

Local lenders often provide competitive rates and personalized service.

Is a HELOC Right for You?

A home equity line of credit mortgage in Indiana can be a powerful financial tool, but it’s not right for everyone.

A HELOC may be a good option if you:

✔ Have significant home equity

✔ Need flexible access to funds

✔ Plan to use the money responsibly

✔ Have stable income to repay the loan

It may not be ideal if you:

✘ Struggle with debt management

✘ Need a fixed payment structure

✘ Are uncomfortable using your home as collateral

Taking time to evaluate your financial situation will help you make the right decision.

Step-by-Step Process to Apply for a HELOC in Indiana

If you decide a HELOC is right for you, here’s what the typical process looks like.

Step 1: Check Your Home Equity

Estimate your home value and subtract your mortgage balance.

Step 2: Review Your Credit

Check your credit score and credit report before applying.

Step 3: Compare Lenders

Look for lenders offering competitive HELOC terms in Indiana.

Step 4: Submit an Application

Provide documentation such as:

- Income verification

- Mortgage statements

- Property information

Step 5: Home Appraisal

Some lenders require an appraisal to confirm your home’s value.

Step 6: Approval and Closing

Once approved, you’ll sign closing documents and gain access to your credit line.

Final Thoughts: Using Your Home Equity Wisely

Your home is one of your most valuable assets, and tapping into its equity can open the door to many financial opportunities.

A home equity line of credit mortgage in Indiana offers flexibility, competitive interest rates, and access to substantial funds. Whether you’re renovating your home, consolidating debt, or preparing for future expenses, a HELOC can be a smart option when used responsibly.

The key is to approach it with a clear plan.

Borrow thoughtfully, compare lenders, and ensure the loan aligns with your long-term financial goals.

If used wisely, a HELOC can be more than just a loan—it can be a powerful financial tool that helps you improve your home, manage your finances, and invest in your future.