There’s something deeply personal about buying your first home.

It’s not just about square footage or mortgage rates. It’s about imagining your mornings there. The smell of coffee in a kitchen that’s finally yours. The quiet satisfaction of turning a key in a door that belongs to you — not a landlord.

But if you’re reading this, you already know the other side of that dream too.

The stress.

The confusion.

The “How am I ever going to afford this?” feeling.

And in 2026, that feeling is very real — even in a relatively affordable state like Indiana.

But here’s the good news:

👉 You are not alone.

👉 And more importantly — you’re not without help.

Indiana actually offers some of the most generous first-time homebuyer programs in the country, and many people don’t even realize what they qualify for.

So let’s walk through everything — slowly, clearly, and honestly — like a friend would.

Table of Contents

🏡 Why Buying in Indiana in 2026 Still Makes Sense

Let’s start with perspective.

Indiana remains one of the more affordable housing markets in the U.S., with home prices still below the national average (). Even though prices have risen in recent years, the barrier isn’t usually the total cost…

It’s the upfront cash.

That down payment.

That one hurdle that makes people feel stuck for years.

But here’s the truth most people don’t hear enough:

👉 You don’t need 20% down.

👉 In many cases, you don’t even need 5%.

There are programs in Indiana right now that can bring your upfront cost close to zero.

💡 What Counts as a “First-Time Homebuyer”?

Before we go further, let’s clear up a common misconception.

You don’t have to be buying your very first home ever.

In Indiana (and most programs), you qualify as a first-time homebuyer if:

✔ You haven’t owned a home in the last 3 years ()

✔ You’re buying in certain targeted areas

✔ You meet income and eligibility guidelines

So if you owned a home years ago but life changed — you might still qualify.

🧭 The Main Source of Help: IHCDA

Almost everything in Indiana starts with one organization:

👉 Indiana Housing & Community Development Authority (IHCDA)

They are the backbone of homebuyer assistance in the state.

They don’t just offer one program — they offer multiple paths depending on your situation.

Let’s break them down.

🏠 1. First Place Program (The Big One)

This is the program most people end up using — and for good reason.

What it offers:

- Up to 6% of the home’s purchase price in assistance

- Can be used for:

- Down payment

- Closing costs

- Comes as a second mortgage

- No monthly payments

- Forgiven after 9 years ()

What that means in real life:

If you buy a $250,000 home…

👉 You could get up to $15,000 in assistance

That’s enough to cover:

- Your entire down payment

- Most (or all) closing costs

And if you stay in the home long enough…

👉 You never pay it back.

The emotional reality

This program is often the difference between:

❌ “Maybe someday”

and

✅ “I can actually do this now”

🏠 2. Next Home Program (More Flexible, Faster Forgiveness)

Not everyone fits into “first-time buyer only” boxes.

That’s where this comes in.

What it offers:

- Up to 3.5% assistance

- Works with FHA loans

- Forgiven in as little as 2–3 years ()

Why people love it:

It’s faster.

You don’t have to wait nearly a decade to feel “free” from the assistance.

💧 3. H2O Program (Helping to Own)

This one is special.

Because it’s not a loan.

It’s a grant.

What it offers:

- Around 3.5% of the loan amount

- Used for down payment

- No repayment required ()

The catch:

- Must be a true first-time buyer

- Usually paired with FHA loans

But honestly?

If you’re struggling to save…

This is one of the most powerful options available.

🧾 4. Mortgage Credit Certificate (MCC)

This one doesn’t help upfront.

But it helps every single year.

What it does:

- Gives you a federal tax credit

- Up to $2,000 annually ()

Translation:

You keep more of your money.

Every year.

For as long as you have the mortgage.

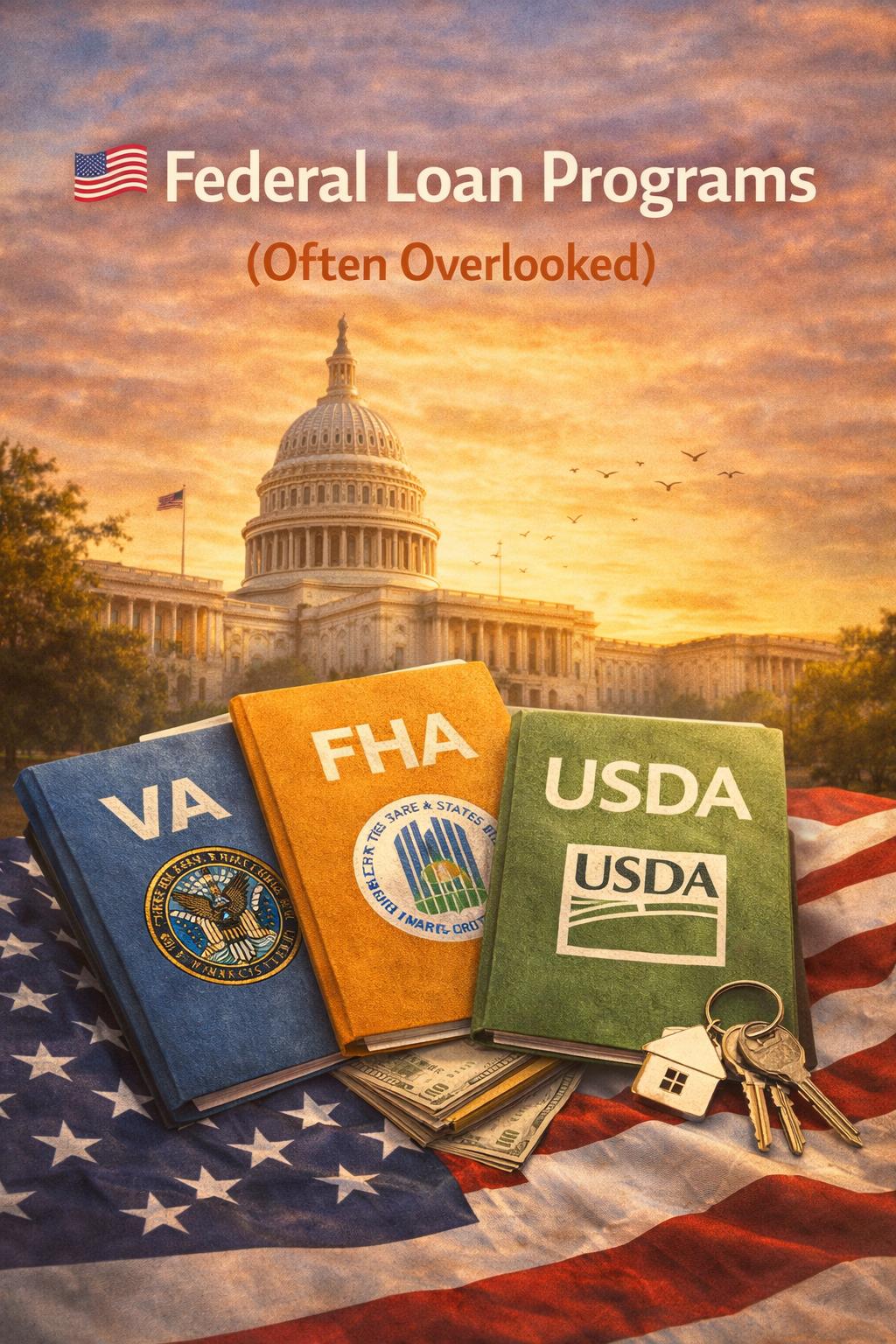

🇺🇸 Federal Loan Programs (Often Overlooked)

Even outside Indiana-specific programs, there are powerful federal options.

And these can be combined with state assistance.

🏦 FHA Loans

- Down payment: 3.5%

- Credit score: as low as 580

- Very beginner-friendly ()

👉 This is the most common starting point.

🌾 USDA Loans

- 0% down payment

- Designed for rural and suburban areas

- Many parts of Indiana qualify ()

👉 Yes — you can literally buy a home with no down payment.

🎖 VA Loans

- 0% down

- No mortgage insurance

- For veterans and active-duty service members ()

👉 One of the best loan options in the U.S.

🏙 Local Programs (Hidden Opportunities)

Beyond state and federal help, cities also offer support.

Examples include:

- Indianapolis assistance programs

- Evansville forgivable loans

- First-generation buyer programs (like HomeBoost) ()

These change frequently — but they can stack with other programs.

😟 The Hard Truth About 2026

Let’s be honest for a moment.

Even with all these programs…

Buying a home still feels overwhelming.

Because affordability isn’t just about the down payment.

It’s about:

- Monthly payments

- Job stability

- Fear of making the “wrong decision”

In some areas, housing costs can take up over 30% of income, pushing affordability limits ().

And that fear?

That hesitation?

It’s normal.

🧭 A Realistic Step-by-Step Plan

If you’re serious about buying…

Here’s what that journey actually looks like:

1. Check your credit

Most programs require around 640, though FHA can go lower ()

2. Take a homebuyer education course

Required for most programs

(And honestly, it helps more than you’d expect)

3. Find an approved lender

Not every lender works with IHCDA programs ()

4. Get pre-approved

This tells you:

- What you can afford

- What programs you qualify for

5. Start house hunting

Now it gets exciting.

6. Apply for assistance

Usually happens once you have a contract on a home

💭 What No One Tells First-Time Buyers

Let’s pause for something real.

Buying your first home isn’t just a financial decision.

It’s emotional.

You’ll feel:

- Excited one day

- Terrified the next

- Confident… then doubtful

That’s normal.

Because this is one of the biggest decisions you’ll ever make.

❤️ The Bigger Picture

Here’s what matters most:

Homeownership isn’t just about owning property.

It’s about:

- Stability

- Independence

- Building something that’s yours

And in Indiana — compared to most states — that dream is still within reach.

Especially in 2026.

🏁 Final Thoughts

If you take nothing else from this guide, remember this:

👉 You don’t need to do this alone

👉 You don’t need perfect finances

👉 And you definitely don’t need 20% down

There are real programs.

Real help.

Real pathways.

And one of them might be exactly what you need.

If you’re even thinking about buying…

Start exploring your options now.

Because sometimes, the biggest step isn’t getting approved.

It’s simply believing:

👉 “This might actually be possible for me.”

And it is. 🏡